The Bright Future Persists: Unlocking Value in the Semiconductor Equipment Supply Chain

Nov 2024

| The semiconductor equipment industry remains a critical enabler of global technological progress. The meteoric market revenue increase of the global semiconductor industry, driven by megatrends, national policies and advancing technology, positions the supply chain as a compelling long-term investment opportunity. That’s why, despite some recent headwinds, we continue to be bullish on this sector. |

Summary

-

Lincoln International experts provide perspective on the future of the semiconductor equipment sector.

- Sign up to receive Lincoln's perspectives

|

|

Mass adoption of transformative technologiesSemiconductors are critical in multiple transformative technologies that are growing rapidly. Lincoln anticipates that the semiconductor market will double in size by 2030, reaching $1,000–$1,300 billion, driven by the following trends:

The industry’s relentless drive toward smaller, faster, and more efficient chips spurs demand for next-generation, technologically advanced manufacturing equipment. |

|

|

Capacity Expansion and National PoliciesTo support market growth, major chip manufacturers—including Samsung, TSMC, and Intel—have launched ambitious capital expenditure programs. Simultaneously, governments are heavily investing in domestic semiconductor production to address supply chain vulnerabilities and strengthen national security: The $52 billion CHIPS Act in the U.S. and the €45 billion European Chips Act in the EU are fostering regional capacity expansion, driving demand for semiconductor equipment beyond traditional chip requirements. |

|

|

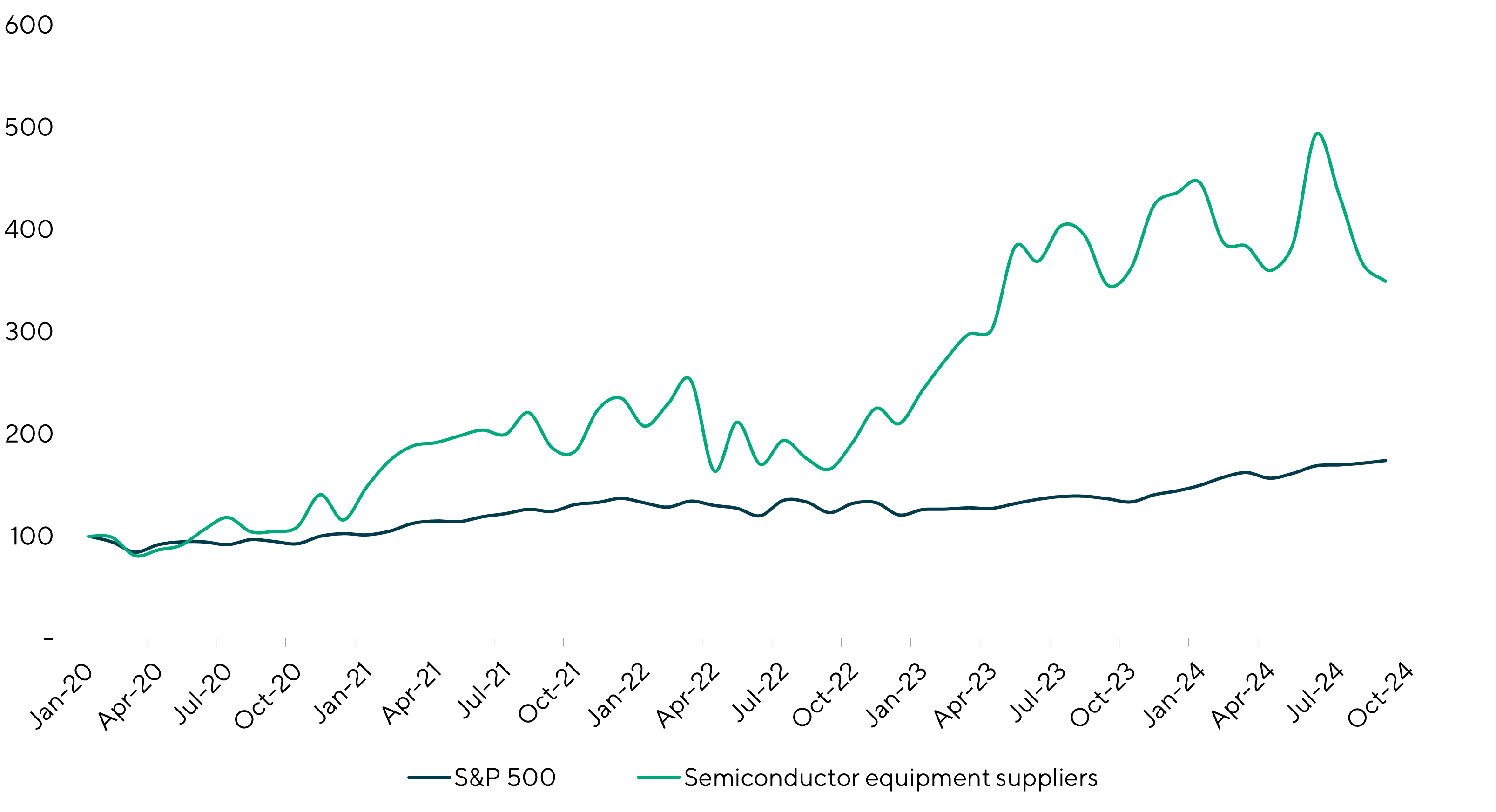

Industry Performance and Recent TrendsShare Price Development of Semiconductor Equipment Suppliers Benchmarked to the S&P 500 (Indexed)

The long-term growth prospects of the semiconductor equipment sector are evident in the stock performance of public suppliers, which have outpaced the S&P 500 over the past five years. However, the industry is currently experiencing a temporary slowdown, influenced by:

|

|

|

Outlook for Recovery and GrowthDespite the short-term headwinds, order books indicate robust growth potential in 2025. Companies across the supply chain are expanding capacity to meet the long-term demand trajectory. For example, wafer fabrication equipment manufacturers are seeing increased interest in next-generation lithography and metrology tools to support advanced chipmaking processes. |

Private Markets Embrace Semiconductor Equipment Opportunities

Driven by its robust growth potential, high margins, and resilient business dynamics, private markets have demonstrated strong interest in the semiconductor equipment sector, with over 30 key private equity-led transactions since 2020.

Key Transactions in the European Semicon Equipment Supply Chain

![]()

Source(s): Lincoln analysis, Gain.pro

Increasing Interest from Private Markets

The significant deal activity in recent years has provided private equity investors with deeper insights into the industry’s fundamentals. Private equity firms are drawn to the semiconductor equipment supplier ecosystem, which supplies key players such as ASML in Europe and Applied Materials, KLA, and Lam Research in the U.S.. These suppliers operate in a high-growth market, strengthened by secular trends like AI, 5G, and the energy transition and consistently deliver EBITDA margins exceeding 20%, significantly higher than the broader industrial average of 11%, and sound cash flows. Such financial performance, combined with long-term growth drivers, makes these businesses ideal candidates for private equity investment.

Private debt and commercial lenders have also increased their exposure to the sector. In the past two years, multiple (re)financings have showcased the sector’s ability to secure favorable terms. This is largely due to its robust fundamentals, with lenders citing recurring revenue streams, predictable growth, and long-term customer relationships as key factors in their decisions.

Outlook for Private Market Activity

Private equity and private debt players are now actively pursuing investments the supply ecosystems of semiconductor equipment OEMs, which include smaller, specialized component manufacturers and service providers. With semiconductor equipment spending expected to reach $190 billion by 2030, the sector remains a high-priority target for private markets.

As private market participants continue to refine their understanding of this dynamic industry, deal activity is expected to remain strong, bolstered by favorable growth trends and proven financial performance across the semiconductor equipment supply chain.

Key Value Drivers in the Semiconductor Supply Chain

The semiconductor supply chain is defined by high-value attributes that ensure its attractiveness to private equity buyers and debt providers:

|

1 |

Mission-Critical ProductsSemiconductor equipment requires components with extremely tight tolerances, often to sub-micron levels, ensuring exact replication across production cycles. Super low tolerances, high customization and “Copy Exact” requirements are vital for extremely precise tools like ASML’s EUV lithography machines, leading to single source supplier relationships. |

|

2 |

Involvement at OEMs from R&D to PurchasingDesign for Manufacturing (DfM): Suppliers collaborate with OEMs early in the product lifecycle, contributing to designs that enhance manufacturability and efficiency. For instance, aligning with its broader strategy of fostering ecosystem collaboration, Applied Materials reports that it works closely with suppliers during prototyping to optimize tools for mass production. Prototyping to Series Production: Suppliers often transition seamlessly from prototypes to high-volume production, ensuring consistency and reliability for the OEM and a locked in position for the supplier. |

|

3 |

Customer Lock-InSingle-Source and Long-Term Platforms: Suppliers are often specified as sole providers for critical components, ensuring long-term partnerships. High Switching Costs and Risks: Due to the precision and complexity of semiconductor equipment, switching suppliers can result in operational disruptions and high qualification costs. |

|

4 |

Intellectual Property (IP)Suppliers with expertise in super-tight tolerances and replicable processes often offer patented solutions that differentiate them in the market and maintain a competitive edge. Even if their products are not patented, suppliers often have proprietary knowledge of the manufacturing process which is nearly impossible to replicate and serves as de facto IP. |

|

5 |

End MarketsMany suppliers specialize exclusively in semiconductors but also demonstrate adaptability in related high-precision and high-growth industries like medical technology, aerospace & defense, and analytical equipment. The shared requirements for precision, cleanliness, and replicability across these markets make them a natural fit for suppliers and/or their investors aiming for diversification. |

|

6 |

Financial ProfileComponent manufacturers in the semiconductor supply chain often achieve EBITDA margins exceeding 20%, significantly higher than other industrial sectors. While investments for growth are required to keep up with the fast growth of the industry, suppliers can confidently invest in capacity expansion to meet future needs based on locked-in customer relationships and predictable demand. |

The Road Ahead: Why Lincoln?The semiconductor equipment supply chain is defined by innovation, complexity, and opportunity. For private equity investors, the focus should be on identifying suppliers with distinctive, scalable technology in attractive nichesand strong customer lock-in. As the demand for semiconductors continues to surge, those who navigate this intricate supply chain with strategic precision will unlock unparalleled growth and value. Lincoln International has an unmatched track record in advising clients within the semiconductor equipment value chain. Driven by our deep understanding and extensive experience we help our clients navigate this complex landscape and deliver exceptional value for our clients. |

Contributors

Meet Professionals with Complementary Expertise in Industrials

I am a rigorous advocate for my clients with a hands-on, communicative approach, focused on delivering intense advocacy and outlier results.

Sean Bennis

Managing Director & Co-head of Industrials

Chicago

I enjoy leading clients and realizing their objectives, while structuring solutions to issues that are both intriguing and challenging.

Øyvind Bjordal

Managing Director | Head of Switzerland

Zurich

Building long-term relationships is key for me personally – I want to be the advisor of trust for my clients.

Dr. Michael Drill

Managing Director | Head of Germany

Frankfurt